Spiral Days

Miguel Lebre de Freitas

The government announces that, from now on, and for saving purposes, the light at the end of the tunnel will be switched off.

Intro

A main problem with large cross border capital

flows is when they stop. During the up-phase, the excess demand over domestic

supply translates into a selective inflation, whereby prices of non-tradable

goods increase and workers acquire purchasing power over imported goods. During

the down-phase, the reverse has to occur. In the case of Portugal, the fact that it

belongs to a monetary union made many people (including me) trust that the down phase would be smooth. But in fact

it wasn’t: after a long period of accumulation of external liabilities, private

capital stopped flowing in abruptly, in the aftermath of the subprime crisis. True, the replacement of

private capital by official lending allowed a smoother transition than

otherwise. Still, the shortage of foreign capital broad sense forced the Portuguese economy

into external balance in a very short period of time.

Looking behind, the adjustment process so far failed to

deliver structural adjustment, in the sense that the labour force released by

contracting industries moved to unemployment (and abroad), rather than being absorbed by

export-oriented green field investment. Exports did increase, but this was largely achieved through a more intensive use of existing capacity. Some analysts interpreted this failure as

a symptom of price and wage stickiness. This view fails however to account

for the fact that, during most of the bailout period, external demand remained weak, access to credit was limited and - most important - Portugal faced one of the most serious confidence crises in its

recent history. In such a context, lack of green field investment should not be

a surprise.

I take opportunity to argue that the tax hike on food service activities was a poor avenue to raise government revenues.

I take opportunity to argue that the tax hike on food service activities was a poor avenue to raise government revenues.

The toy story

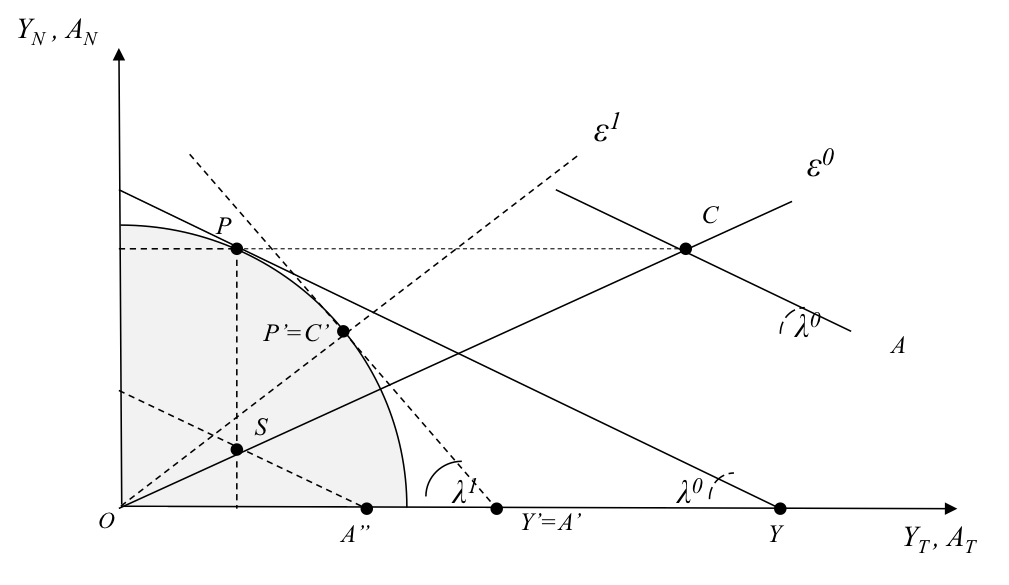

To make the point on VAT, I need a couple

of graphs (don't worry: I just copied and pasted from my class-notes). This is a baby version of the dependent

economy model without inter-temporal substitution effects and other

complications. Figure 1 plots the country production possibilities frontier, domestic

absorption and preferences (as implied by linear income expansion paths),

splitting the economy into tradable (T) and non-tradable goods (N). In the Figure, take (P,C) as the situation at the outset of the adjustment process, with domestic absorption (A) exceeding the value of

output (Y). In that stage, consumption occurs in C and production in P, and the

horizontal distance between P and C measures the external imbalance (for

simplicity, we start out with internal balance).

Then, consider the case where a major international

portfolio rebalancing causes borrowing constraints to become binding to everyone

in this economy, so that the aggregate is forced into external balance (one could discuss the case of a primary surplus, but that would not make much difference). In the

figure, this is represented by a contraction of domestic absorption from A to

A’.

Figure 1. External adjustment with sticky wages

The well functioning case

In a well functioning economy, price flexibility would ensure that the relative price of tradable goods (lambda) increased. This would favour the macroeconomic adjustment, by inducing:(a) Households to switch consumption away from tradable goods towards non-tradable (the income expansion path would become steeper);

(b) Firms to reallocate employment towards tradable goods.

The new equilibrium would be reached at P’=C’, with internal and external balance.

(Note that, since the value

of domestic output in terms of tradable goods declines from Y to Y’, external

debt as a percentage of GDP jumps up; in a World with financial market frictions, the implied balance sheet effect should weigh negatively on domestic absorption).

The case with sticky prices

In the absence of an exchange rate

mechanism, a capital flow reversal poses a major policy challenge: how to

achieve the downward adjustment of wages and prices. If these fail to respond,

economic recovery may become conditional on foreign inflation, implying a slow

and painful adjustment process with high unemployment.

The case with nominal stickiness is described in Figure 1 by point S. In this case, nominal wages and non-tradable good prices fail to decline, so the slope of domestic absorption remains unchanged. Thus, production of tradable goods remains stuck in P, consumers remain attached to the original Engel curve and domestic absorption is required to fall much more in order to meet the external balance (A’’). In the new consumption point (S), the demand for non-tradable goods falls short the potential supply (P), so unemployment soars up, proportional to the distance between S and P. Employment fails to be absorbed by tradable good industries, because firms don’t see the relative price of tradable goods increasing. In the non-tradable goods sector, the employment contraction overshoots what is required in the long run.

Point S illustrates the typical case of a “sudden

stop” under fixed exchange rates and sticky prices. A popular example in this

category is Chile at the time of the second oil shock, when generalized wage indexation prevented

relative prices from changing. In the case of Portugal, there is also a view

that the failure of wages and prices to decline is the fundamental

explanation for the painful adjustment path along 2010-2013.

An alternative view

Sticky prices is not

the only possible explanation for the failure of export oriented investment and employment to spring up. Another candidate is the theory that entrepreneurs, perceiving an unusually risky

environment, low external demand, and high borrowing costs, mostly decided to wait and see. On the financial side, highly leveraged banks with little margin of manoeuvre, found reasons to redirect the scarce loanable funds to the rolling over of debts of large borrowers banished from capital markets (including the government and SOEs), away from new entrepreneurship, which risk is more costly to assess. With low investment demand and low availability of credit, the production structure remained temporarily frozen, as determined by past investments minus current bankruptcies

This case is

described in Figure 2. Figure 2 is similar to Figure 1, except that firms refrain from hiring and investing, so inputs cannot actually move across sectors. Thus, the potential pattern of production remains unchanged, regardless of relative prices (in the figure, this is illustrated by the rotation of producer prices around P).

The adjustment in this case is observationally similar to that in Figure 1: since employment in tradable goods does not expand, the external balance has to be meet somewhere in the vertical line below P in the direction of S. The actual short term equilibrium will depend on consumption prices: if consumer prices don’t change at all – like in Figure 1 – then external balance will be met at the very same point S; if consumer prices succeed in adjusting in the right direction, external balance will be met somewhere above S, in the direction of P: this will allow unemployment to be reduced, though not eliminated.

The adjustment in this case is observationally similar to that in Figure 1: since employment in tradable goods does not expand, the external balance has to be meet somewhere in the vertical line below P in the direction of S. The actual short term equilibrium will depend on consumption prices: if consumer prices don’t change at all – like in Figure 1 – then external balance will be met at the very same point S; if consumer prices succeed in adjusting in the right direction, external balance will be met somewhere above S, in the direction of P: this will allow unemployment to be reduced, though not eliminated.

Figure 2. External adjustment with unresponsive supply

Fiscal revaluation

In figure 2, I describe by point T the case in

which consumer prices move in the wrong direction: from S to T, the relative

price of tradable goods declines instead of increasing, causing

the income expansion path to rotate further down, and the external balance to be

met at a higher unemployment level (TP>SP).

This case intends to capture the government decision of increasing the value added tax rate on food service activities: as this causes home good prices to increase in consumption, households are induced to switch expenditure further away from domestically produced goods towards foreign goods, causing unemployment to increase even more. Note that this effect also works in the case of Figure 1: irrespectively as to whether the unemployment problem was caused by price stickiness or investment freeze, the tax hike on restaurants acted as a fiscal revaluation on the consumer side, deepening the recession.

Of course, accounting identities tell us nothing about causality. But the broad idea that a sharper than expected contraction of foreign lending coupled with larger than expected government deficits translated into a huge crowding out of private consumption and investment should not be entirely out of reality.

Table 1: Gross savings and investment, 2011-2013, billion euros

This case intends to capture the government decision of increasing the value added tax rate on food service activities: as this causes home good prices to increase in consumption, households are induced to switch expenditure further away from domestically produced goods towards foreign goods, causing unemployment to increase even more. Note that this effect also works in the case of Figure 1: irrespectively as to whether the unemployment problem was caused by price stickiness or investment freeze, the tax hike on restaurants acted as a fiscal revaluation on the consumer side, deepening the recession.

Crowding out

Table 1 shows the IMF estimates of savings and investment as of June 2011, compared with the revised figures at the time of the 8th/9th review. These figures show that the external adjustment was much sharper than initially forecasted: in June 2011, the IMF estimated the current account to reach a deficit of €7.1bn in 2013, but the reality was a €1.7bn surplus. Along 2011-2013, the cumulative difference amounted to €21.1bn. At the same time, government savings underperformed relative to the initial plan by some €11.4bn, cumulative (this figure does not include SOEs outside the budget perimeter).Of course, accounting identities tell us nothing about causality. But the broad idea that a sharper than expected contraction of foreign lending coupled with larger than expected government deficits translated into a huge crowding out of private consumption and investment should not be entirely out of reality.

Table 1: Gross savings and investment, 2011-2013, billion euros

Source: IMF, Country report, June 2011 and 8th-9th reviews, Oct 2013.

Source: IMF, Country report, June 2011 and 8th-9th reviews, Oct 2013.

Source: IMF, Country report, June 2011 and 8th-9th reviews, Oct 2013.

Spiral fear

During most of the bailout period, Portuguese citizens shared a sentiment of fear about the future that naturally born out of severe austerity, but which political leaders and opinion-makers actually managed to feed, by discrediting the stabilization strategy. This includes most of the political sphere in Portugal, and - notably - the IMF, which looked like plagued with bipolar disorder.

As for the general public, the message that the therapy could actually be killing the patient created a sentiment that the sacrifices imposed were useless. In a short period of time, the initial credential, consisting in a large political and social consensus around the MoU was eroded. In the media, the floor was opened for opinion makers and interest groups to show up and toll on discontentment, turning the policy design increasingly more challenging, each time a major initiative was ruled illegal by the Constitutional Court.

Low social and political support, a narrow legal space and a track record of fiscal slippages amended by one-off measures, helped maintain a sentiment of exposure of taxpayers to the risks of extraordinary taxation, that obviously did not help investment and employment to recover.

As for the general public, the message that the therapy could actually be killing the patient created a sentiment that the sacrifices imposed were useless. In a short period of time, the initial credential, consisting in a large political and social consensus around the MoU was eroded. In the media, the floor was opened for opinion makers and interest groups to show up and toll on discontentment, turning the policy design increasingly more challenging, each time a major initiative was ruled illegal by the Constitutional Court.

Low social and political support, a narrow legal space and a track record of fiscal slippages amended by one-off measures, helped maintain a sentiment of exposure of taxpayers to the risks of extraordinary taxation, that obviously did not help investment and employment to recover.

What now?

In the second half of 2013, there was an inflexion in the Portuguese people’ collective mood. This change followed the improvement in global conditions and had been already reflected in high frequency indicators before, but it was really when the media started echoing the first signs of recovery that the spiral word was banished from the opinion makers' lexicon.

As for the future, the brighter economic environment will come along with renewed exporting opportunities, higher willingness on the part of entrepreneurs to invest and hopefully the easing of credit conditions. Eventually, constraints that were not the most binding in the stage before will show up, slowing down the adjustment process. Whether this will be price stubbornness, low competition, labour market mismatches, energy costs, or the continuing drainage of limited loanable funds by the government deficit, I don't know.

What we know is that the challenges ahead on the fiscal side are still immense: at the completion of the adjustment program, the fundamental question - “who is going to pay what?” - is still plenty of blank spots, urging answers of the permanent type. And yet, the prospects of recovery are coming along with a lower willingness on the part of citizens to accept more sacrifices.

As for the future, the brighter economic environment will come along with renewed exporting opportunities, higher willingness on the part of entrepreneurs to invest and hopefully the easing of credit conditions. Eventually, constraints that were not the most binding in the stage before will show up, slowing down the adjustment process. Whether this will be price stubbornness, low competition, labour market mismatches, energy costs, or the continuing drainage of limited loanable funds by the government deficit, I don't know.

What we know is that the challenges ahead on the fiscal side are still immense: at the completion of the adjustment program, the fundamental question - “who is going to pay what?” - is still plenty of blank spots, urging answers of the permanent type. And yet, the prospects of recovery are coming along with a lower willingness on the part of citizens to accept more sacrifices.

In this context, a political agreement involving the main political parties regarding the drivers and boundaries of the future fiscal strategy would certainly help.

Until a scenario of fiscal stability becomes credible and perceived to be politically feasible by tax payers and bondholders, economic growth will keep facing strong headwinds.

Until a scenario of fiscal stability becomes credible and perceived to be politically feasible by tax payers and bondholders, economic growth will keep facing strong headwinds.