The ongoing negotiations between the Greek government, the troika of official institutions, and the private creditors have failed so far to produce much, apart from increasingly inflamed rhetoric. The sitting Greek prime minister calls them a ‘moment of truth,’ while Jean-Claude Juncker, the leader of the Ecofin, delivered this weekend what amounts to an

ultimatum to the Greek government.

It is perhaps fitting that yet another round of bargaining should take the tones of a Greek tragedy, but both sides seem to be dangerously over-playing their cards and run the risk of getting cornered into a position from which they may not be able to back-track. All of this brings back old memories, which are still instructive to interpret the current situation.

Greece is no newcomer to sovereign default. In fact, it spent almost half of its time as a sovereign nation in a state of default – the last one settled as recently as 1964. It is also not the first time that this country has been bailed out by its northern European partners. Greece was the beneficiary of what were probably the first two Eurobonds in history. To the proponents of this solution for the European debt crisis, the record of these two bonds offers some cautionary lessons.

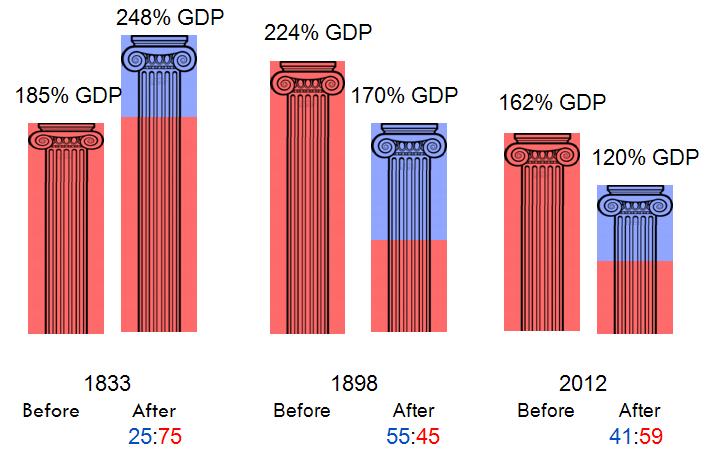

After a long emancipation war, Greek independence was recognised by the Ottoman Empire in 1830. The then main European powers were instrumental to this outcome by effectively insuring Greek independence by treaty. They also funded the start up costs of the new nation with a £1.6 million loan, issued in 1833 under the several guarantee of Britain, France, and Russia. Under the agreement each power guaranteed half a million of the loan separately. Thanks to the guarantee, the new Greek nation was able to finance itself at barely 1% above the cost of borrowing for the three powers. In exchange, the powers demanded that these bonds would be senior to all previous Greek debt, raised privately to fight the independence war. This structure was remarkably similar to the Delpla-Weizsäcker proposal to divide the debt of European governments between ‘blue bonds,’ jointly guaranteed by all Eurozone nations and ‘red bonds,’ which remained the sole responsibility of each nation. In the Greek case the split was 25% blue to 75% red, adding to a massive 248% of GDP. The recent proposals for the Eurozone hark back to the debt criterion of the Maastricht treaty and propose instead a 60:40 split.

Figure 1: Greek sovereign yields, 1832

The vertical line marks the announcement of the guaranteed loan

Unfortunately, and as feared by the critics of the Eurobond proposal, one of the first consequences of the 1833 guaranteed bond was to make the remaining Greek debt unpayable. After almost a decade of war, the Greek government had no intention of pressing ahead with the tax increases needed to make good the payments on its debt. This was reflected in the yields of the old red bonds (Figure 1). After falling, in expectation of a comprehensive debt agreement, the yields rose back again to close to 20% once the details of the guaranteed bond were known. The Greek government would remain in default on its red debt until 1879! The first lesson from history is therefore that no Eurobond has a chance of success without a private sector involvement (PSI), a point only admitted since last October at German insistence, and after two failed bailout plans.

By 1839 the Greek government had also defaulted on the official blue debt, despite its supposed senior status. After a long series of efforts by the guaranteeing powers, that involved a revolution, a naval blockade, and a change of ruling dynasty, a final settlement was reached in 1864. By then the UK had paid £1.2 million of service for its share of the Greek debt, against a contribution by the Greeks of no more than £100,000. The second lesson is that just because no country ever defaulted on IMF debt that does not mean that defaults on official debt are impossible.

Thirty years and another war later, the Greek state defaulted again on a pile of debt worth 224% of GDP. The same powers intervened again and granted another guaranteed loan, issued in 1898 at the very low 2.5% interest rate. This time, however, they had learnt the lesson of moral hazard and insisted on the involvement of the private sector, which accepted a 61% cut of the original debt obligations, a value halfway between the 50% originally negotiated last October and the 70% now apparently being considered in Athens. This resulted in a drop of the total debt to 170%, split 55:45 between blue and red bonds (Figure 2). More significantly, the creditor nations forced the Greek government to limit its borrowing from the central bank and to accept the imposition of an ‘International Control Commission’ (ICC) which managed a series of domestic taxes and revenues to ensure that foreign creditors were paid before any other claims on the public purse. This deal was a relative success. Under the supervision of the ICC, Greek finances were reined in, and foreign capital was attracted back to the country, which helped with a rapid economic recovery in the years leading up to World War I. The German insistence for an independent ECB and the suggestion last week to introduce a ‘state commissioner,’ representing the European Union in Greece and with veto power on fiscal policy, clearly seem to echo the 1898 settlement.

Figure 2: Three defaults compared (government debt/GDP)

Perhaps, instead of “the product of a sick imagination,” as the Greek Education Minister defined it, the most recent German plan may be a consequence of the high degree of historical awareness in that country! If so, the history-conscious Germans should take heed of the dangers in using wrong historical analogies as a guide for policy. And this leads me to the third lesson. In 1898 Greece only accepted to surrender its fiscal sovereignty to the ICC as a counterpart to the settlement of a disastrous war and at a time when Ottoman troops still occupied the north of the country. In other words, the value of the status quo was very negative and the Greeks had no real choice but to accept the deal imposed by the guaranteeing powers. Today, the successive rounds of austerity imposed on the Greeks as counterpart for the release of outside help risk eroding the internal option of remaining within the framework of the troika negotiations.The temptation of going their own way correspondingly increases.

The Greeks might be recalled of the trials of Sisyphus and imagine themselves as being compelled to roll a heavy rock up a hill, only to watch it roll back down, and having to start again. Will they wait until eternity?