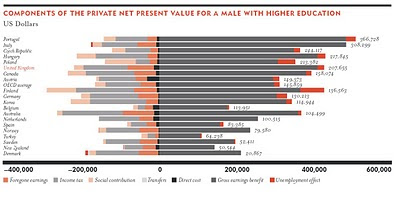

Figure 1

The UK received this week, not without some trepidation, the conclusions from the so-called Browne report on higher education and student finance in England. As was long expected, the review committee recommended an end to the cap on university fees, currently £3,290 per year (€3,800). The report suggests that different universities should charge different fees and, in particular, that world-class institutions should be allowed to charge much higher fees from their students, possibly above £12,000 (€13,800) per year. The report justifies this proposal for increased private contributions as a necessary means “to support high quality provision and allow the sector to grow to meet qualified demand.” The current budget crunch added to the urgency of these conclusions, as the country braces itself for the comprehensive spending review due next week. Today’s newspapers rumoured that the government is set to cut up to 80% of the public funding of university teaching, which would leave UK universities in serious financial strictures.

Earlier in the year, the results of the university admission exercise revealed that more than 150,000 applicants would not get a place, out of a total of 660,000. In the face of such excess demand for university places, elementary economics would suggest that some price rationing was in order. Some politicians, parents’ and students’ representatives have contended that a fee hike would unfairly saddle students with a heavy debt burden at the beginning of their working lives. Furthermore, fees of £12,000 or more would surely dissuade bright or otherwise aspiring pupils with an underprivileged background from applying at all.

The authors of the report disagree and take particular pains at arguing how this dissuasion effect can be avoided. One of the reasons is that graduates can pay more for their education. How much more? The authors rightly leave that to the market, while noting that “compared to other countries, high numbers of students in England complete their degrees and go on to employment with an earnings premium that is high by international standards.” This “earnings premium” is measured as the net benefit (in lifetime earnings) from completing a degree over the expected life-long remuneration of an individual who enters the job market with a high-school diploma. According to the data in Figure 1, this premium in the UK stands at slightly above 200,000 US dollars (€150,000) for a male with higher education. This is a third higher than the OECD average.

We all know the debate, as it has been rehearsed several times in Portugal since 1992. What I found interesting in the report was the oblique reference to Portugal as an outlier in the context of OECD countries. Portuguese university graduates have a staggering relative advantage over their non-degree holding competitors in the labour market. We currently lead the OECD in both net and in gross benefits from higher education. A university education is worth today €265,000 in Portugal, fully 2.5 times the OECD average.

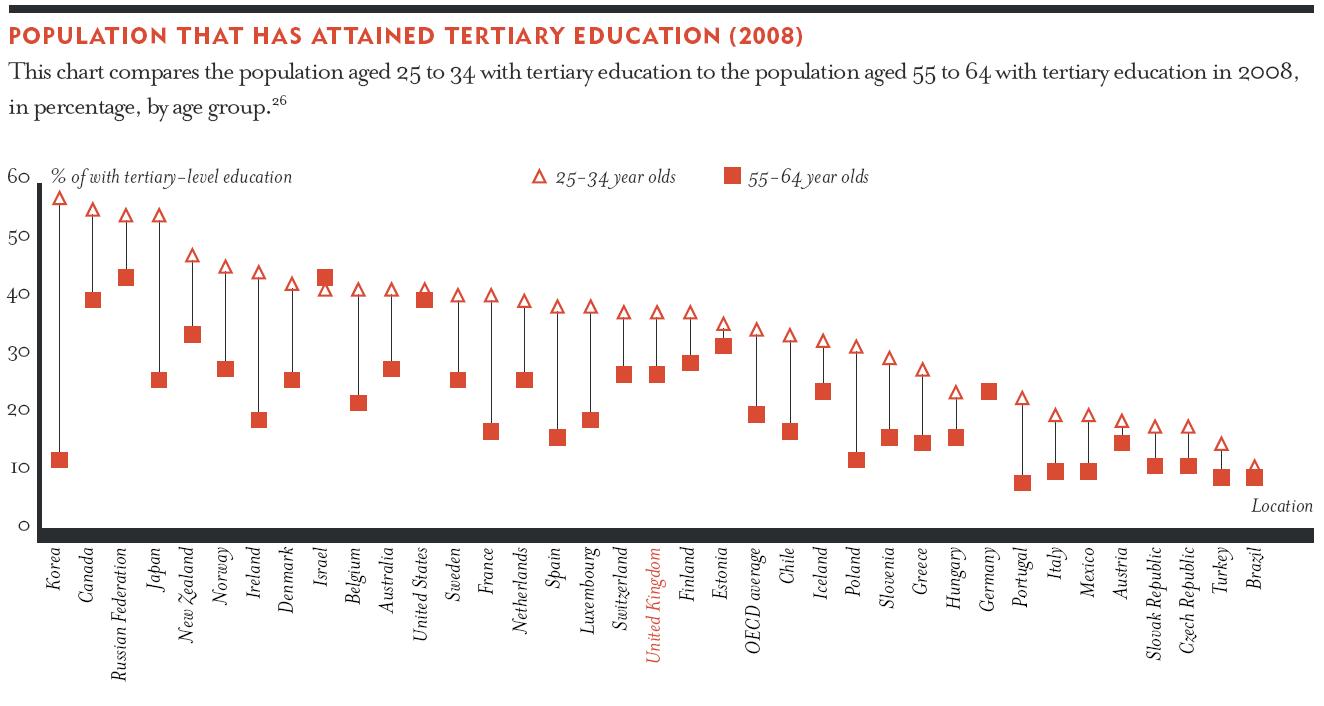

This is clearly not a matter to be proud of. As a university lecturer myself, I refrain from commenting on what a fee hike from the current €920 could represent for the quality and growth of Portuguese universities. But I cannot but see the connection between a very high “earnings premium” and the low fraction of the population that has attained a university degree (Figure 2). Contrary to a contemporary current of opinion, there may not be “too many graduates” looking for inexistent jobs, but too few.

Figure 2

And here is another connection. A very interesting book recently singled out Portugal as an outlier, again for the wrong reasons. The authors of The Spirit Level notice that by level of income inequality, Portugal comes second among OECD economies, just after the USA... Most economists will agree that access to education is a powerful equalizer of opportunities, and that, vice-versa, a restrictive university system is a certain way of perpetuating income (and social) inequalities, particularly in our current skills-intensive model of economic growth. How one may go about increasing access to tertiary education is another question (namely in terms of how to split the cost between the state and the students), but the weight of evidence about the consequences of not doing so cannot be ignored.

{kind=link}

{kind=link}